(Bloomberg) — Stocks fluctuated after data showed hotter-than-expected inflation and a slowdown in the labor market, highlighting the Federal Reserve’s challenges after it started bringing rates down last month.

Most Read from Bloomberg

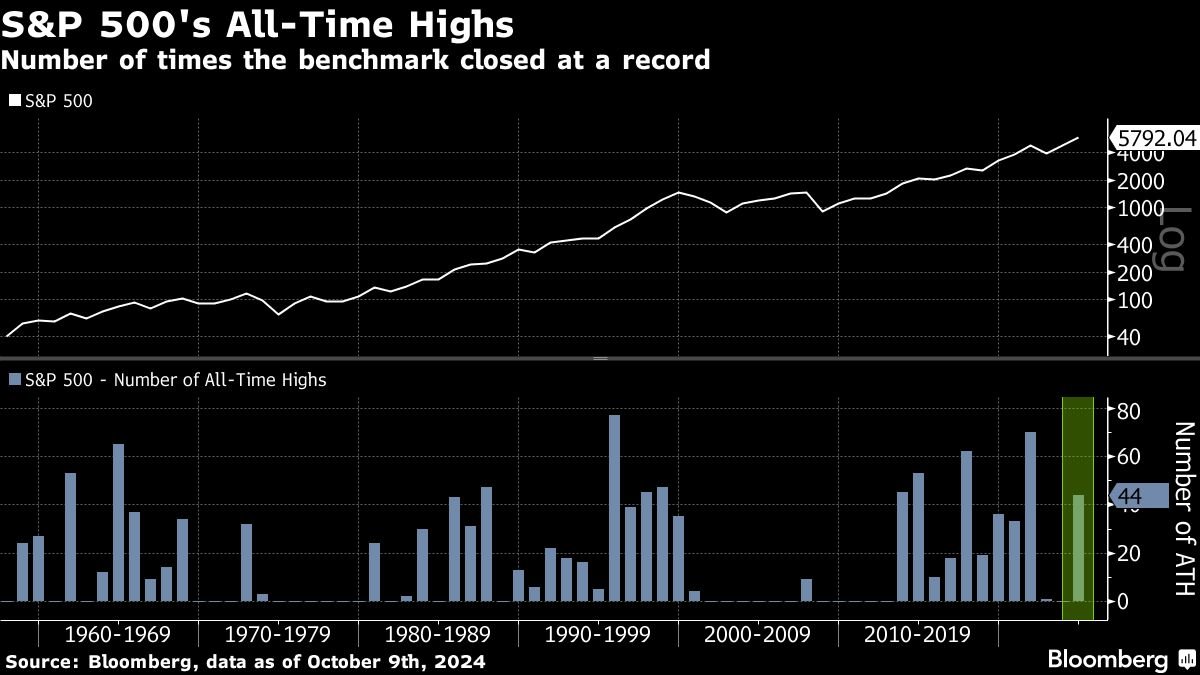

Following a rally to all-time highs, the S&P 500 struggled to gain much traction. While Thursday’s economic figures were not perceived by Wall Street as catastrophic, they certainly added to the debate on the Fed’s next steps. For now, bond traders only reinforced bets the central bank will reduce the pace of cuts to 25 basis points in November.

The so-called core consumer price index — which excludes food and energy costs — increased 0.3% from August and 3.3% from a year ago. Meantime, applications for US unemployment benefits rose last week to the highest in over a year, reflecting large increases in Michigan, as well as states affected by Hurricane Helene.

In a note titled “The Fed’s quandary as inflation warmer while labor cooler,” Quincy Krosby at LPL Financial says the latest economic numbers were not the combination the Fed wants to see.

“If inflation data continues to indicate that prices are generally rising amid a backdrop of a cooler labor market, the Fed’s next meeting will undoubtedly involve a more heated discussion of which of the Fed’s mandates takes precedence.”

Fed Bank of Chicago President Austan Goolsbee stuck by his view that the central bank has moved past its singular focus on price pressures. His New York counterpart John Williams said policymakers should reduce rates toward a more neutral level “over time” now that the risks to achieving both their inflation and employment goals are better balanced.

“The Fed said the last mile getting toward their inflation target is going to be tough, and that is what we are seeing,” said David Donabedian at CIBC Private Wealth US. “But we still expect the Fed to cut rates by a quarter point in November, and likely a similar cut at the December meeting.”

The S&P 500 was little changed. Most major groups retreated, though energy shares joined oil higher as speculation about Israel’s response to the Iranian missile attack continued to whipsaw the market. Megacaps were mixed, with Nvidia Corp. up and Apple Inc. down. Tesla Inc. fluctuated as investors awaited the first look at the company’s fully self-driving vehicle later Thursday.

The yield on 10-year Treasuries were little changed at 4.08%. The Bloomberg Dollar Spot Index wavered.

Wall Street’s Reaction:

Today’s CPI report will lower enthusiasm around rate cuts next month, and if some of these other catalysts increase uncertainty, it could act as a short-term excuse for markets to pull back — particularly with the S&P 500 at all-time highs.

If investors are looking for a silver lining, it’s this: Despite this morning’s disappointing jobless claims data, worries over the labor market eased with last week’s strong jobs report. While lower inflation is the goal, falling off a cliff may cause some concern about the economy. One report doesn’t make a trend, but the US economy appears to be on solid footing. We’ll turn our attention to the retail sales report and to earnings to get better insights on the health of the consumer.

If anything, the report was good enough to solidify the case for another quarter-point cut. Inflation hasn’t receded so rapidly to justify an accelerated pace of policy easing, but the upside surprise also wasn’t sufficient to raise serious questions about the underlying disinflationary trend.

The Fed is likely to continue to cut short-term interest rates at the next decision in November, but this time by just a quarter percent, not the half-point cut they made in September. The Fed is glad inflation is getting close to their target, but they would like to see core inflation slow further to be more confident that the slowdown in inflation will persist into 2025.

The Federal Reserve isn’t yet in position to declare ‘mission accomplished’ in the battle against inflation, and the ride to the 2% target continues to be bumpy at times.

Mindful of its dual mandate prioritizing maximum employment and stable prices, it will be eager to see the next monthly jobs report in early November before the next announcement on rates. A safe bet for now is rate reductions of one-quarter of 1% at the final two meetings of the year.

Disinflation continues, but anyone who thought the Fed was going to lower rates by another .50 basis points in November is dead wrong.

When interest rates aren’t high enough to lower growth, they aren’t high enough to stifle inflation completely either. The Fed will lower rates, but at a measured pace from here.

This number might not be as bad as it looks because shelter slowed sharply. That’s important because housing costs have been the biggest lingering issue for inflation. It’s not great news overall, but it’s also unlikely to have much impact because the Fed is still early in its easing cycle. The days of CPI triggering major volatility could be fading.

One slightly hotter-than-expected CPI reading doesn’t mean a new wave of inflation has been unleashed, but the fact that it accompanied a jump in weekly jobless claims may add to short-term market uncertainty.

We’re in a “good news is good, bad news is bad” environment, and these weren’t good numbers — but that doesn’t mean they upended the larger outlook for solid economic growth and moderate inflation.

It’s hard to know if it’s US jobs data or CPI that is more important overall, but today it’s undoubtedly the CPI as it came in a little higher than expected, particularly core inflation. However, this shouldn’t be enough to worry markets or indeed the Fed.

Although there’s more data to be released before the next Fed meeting, this will probably firm up views that a 0.25% cut is appropriate.

The response in the Treasury market has been mixed with the initial rally faded and yields effectively unchanged at this point. We’re certainly sympathetic to the challenge of trading the cross currents of sticky core inflation with rising jobless claims. From here, the market is likely to consolidate in the current range ahead of this afternoon’s long-bond auction.

The Fed has shown that they’re willing to let inflation potentially run hotter than normal in favor of full employment. Only a rise towards 4% inflation or a few hot inflation prints in a row would alter the Fed’s course of continued rate cuts over the next year.

Given that the most recent jobs report was so strong, it was possible that a big upside surprise to inflation could have caused the Fed to pause at the next meeting and leave rates unchanged.

However, given that this month’s report was a little higher than expected it is still likely that the Fed will go ahead and cut by 25 bps next month and – if nothing in the labor market or inflation readings materially changes by the end of the year – another 25 bps in December.

We think investors should be reassured that the economy is doing well, the labor market and consumer spending are both holding up well, and there doesn’t appear to be any signs of recession. It’s possible that the market will be disappointed that the Fed isn’t cutting more rapidly, but we have always said that people should be careful for what they wish for, because an environment which caused the Fed to cut in an extremely rapid manner is probably one where economic weakness (or outright recession) would overshadow the Fed’s rate cuts and cause the stock market to fall even faster.

Economic data just hit the tape, and each report went in the “wrong direction” in terms of the economic impact. CPI data came in higher than expected on both a headline and core basis. Jobless claims, on the other hand, surpassed expectations.

The September CPI report came in stronger than expected, with core CPI in particular surprising to the upside. Labor market data, however, remains in the driving seat for the Fed and we see next month’s payrolls release as the more important data point in determining the pace and extent of Fed easing.

The market reacted negatively to recent indications from policymakers that the next cut would be 0.25%, however, history tells us that consecutive dramatic rate cuts tend to come about when the economy is in distress, so while we expect a cut next month, investors may be wise to hope for a gradual drop.

A fairly stable CPI report, nothing here to sway the course of the Fed’s rate-cutting plan.

While CPI came in slightly higher than expected, it’s still a relief it wasn’t worse. Seeing shelter costs moderate finally is also a relief. The Fed is likely to cut 25 basis points.

Corporate Highlights:

-

Delta Air Lines Inc. forecast profit and sales short of Wall Street’s estimates for the final months of the year, suggesting a slow recovery from a challenging summer travel season.

-

Domino’s Pizza Inc. trimmed its 2024 projection for sales growth and new locations as slower consumer spending hits the restaurant industry.

-

Pfizer Inc. company officials threatened legal action against two former top executives who had been working with Starboard Value to push for changes at the drugmaker, the activist investor alleged Thursday in a letter to the company’s board.

-

GXO Logistics Inc., the supply-chain services provider that spun off from trucking company XPO Inc. in 2021, is exploring a sale, according to people familiar with the matter.

-

Eli Lilly & Co. is ramping up its legal campaign against companies that were temporarily allowed to make and sell copycat versions of its blockbuster drugs used for weight loss until a US shortage ended last week.

-

Toronto-Dominion Bank will pay about $3 billion in penalties and face restrictions on its US growth in a settlement with regulators over its failure to catch money laundering, the Wall Street Journal reported.

Key events this week:

-

JPMorgan, Wells Fargo kick off earnings season for the big Wall Street banks, Friday

-

US PPI, University of Michigan consumer sentiment, Friday

-

Fed’s Lorie Logan, Austan Goolsbee and Michelle Bowman speak, Friday

Some of the main moves in markets:

Stocks

-

The S&P 500 was little changed as of 12 p.m. New York time

-

The Nasdaq 100 was little changed

-

The Dow Jones Industrial Average fell 0.2%

-

The Stoxx Europe 600 fell 0.2%

-

The MSCI World Index was little changed

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro fell 0.1% to $1.0925

-

The British pound fell 0.1% to $1.3053

-

The Japanese yen rose 0.5% to 148.57 per dollar

Cryptocurrencies

-

Bitcoin rose 0.6% to $60,740.91

-

Ether rose 2% to $2,401.41

Bonds

-

The yield on 10-year Treasuries was little changed at 4.08%

-

Germany’s 10-year yield was little changed at 2.26%

-

Britain’s 10-year yield advanced three basis points to 4.21%

Commodities

-

West Texas Intermediate crude rose 2.9% to $75.38 a barrel

-

Spot gold rose 0.6% to $2,624.01 an ounce

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.